Decode crypto claims vs reality for safer trading

Crypto platforms have become extraordinarily skilled at presenting reassuring signals: proof-of-reserves pages, transparency badges, tokenomics whitepapers, and third-party attestations that suggest your funds are safe and the platform is solvent. Yet many of these claims can fail to represent real-world availability, solvency, or the protections users actually need when things go wrong. The gap between what platforms promise and what they genuinely deliver is wider than most traders realise, and navigating that gap requires a more precise analytical framework than simply checking for a badge on a homepage.

Table of Contents

- How crypto platforms construct their claims

- Limitations of proof-of-reserves and transparency features

- Regulation, legal rights and how claims really work

- Checklist for evaluating claims and platform safety

- What most guides get wrong and how to truly safeguard your funds

- Safeguard your investments with independent reviews

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

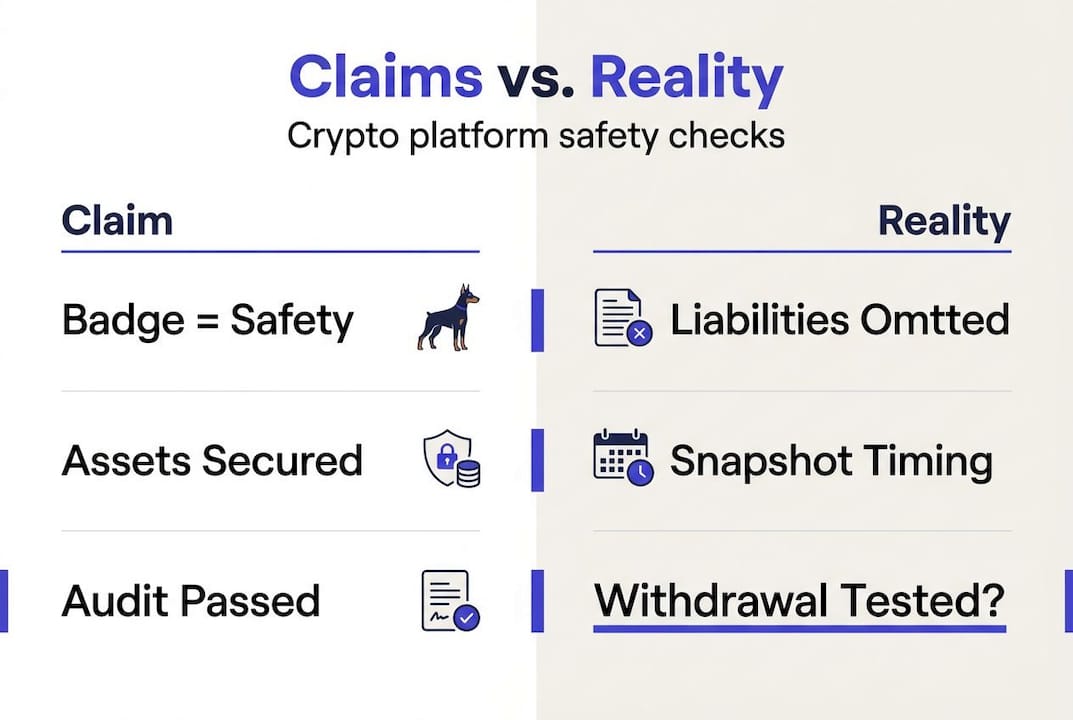

| Badge does not equal safety | Proof-of-reserves and transparency badges often lack key solvency and liability detail. |

| Legal rights vary | Reserve-backed claims rarely mean you have direct redemption access or bankruptcy protection. |

| Check audit depth | Always confirm whether assurances are limited, full audits or simple snapshots. |

| Operational access matters most | Withdrawal history and operational availability are stronger evidence than claims or badges. |

| Practical checklist is essential | Use a comprehensive checklist to scrutinise crypto platform claims before investing. |

How crypto platforms construct their claims

Having set the stage for why crypto claims can mislead, it is worth exploring exactly how platforms manufacture and present these assurances in the first place.

The most prominent example is proof-of-reserves (PoR), a process where a platform publishes on-chain wallet balances, often accompanied by a Merkle tree proof, to demonstrate it holds assets matching user deposits. It sounds rigorous. The problem is that PoR is almost always a snapshot of a single moment, and it addresses only one side of the balance sheet. Liabilities, lending positions, and operational debts are typically absent from the picture entirely.

Transparency badges are a related but even vaguer category. These are third-party seals or self-proclaimed icons that signal compliance, security, or audit status. In practice, the standards behind these badges vary wildly. Some reflect genuine independent verification; others are little more than marketing artefacts that platforms display to build psychological confidence.

Tokenomics claims deserve particular scepticism. When a platform publishes a vesting schedule, supply allocation, or burn mechanism, it is presenting a model of how its native token should behave. What it rarely discloses is what happens if the team alters those parameters, accelerates unlock schedules, or issues new supply through governance mechanisms. Tokenomics narratives are projections, not contractual guarantees.

There is also a critical distinction between spot accounts and margin, futures, or earn accounts that most users overlook. Spot balances are one thing; assets locked in yield products or collateralising margin positions are another. The crypto platform transparency frameworks that cover spot balances alone offer only a partial view of where your assets actually sit and under what conditions they could be frozen, rehypothecated (used as collateral by the platform itself), or locked during stress events.

"Many crypto platform claims can fail to represent real-world availability, solvency, or user protections — particularly when the evidence is limited to snapshot-based reserve pages that exclude liabilities."

What marketing claims most commonly omit includes the following:

- Total liabilities: user deposits in all products, counterparty obligations, and operational debts

- Asset encumbrance: whether reserves are pledged, lent, or otherwise committed elsewhere

- Audit scope and assurance level: whether a third party conducted a limited engagement or a full statutory audit

- Redemption terms: the precise conditions under which you can actually withdraw

Understanding platform trust and security means learning to ask what a claim does not tell you, not just what it does.

Limitations of proof-of-reserves and transparency features

After understanding the types of claims, it is crucial to confront the specific weaknesses that are inherent in the supporting features behind them.

PoR methodology commonly misses key edge risks because it may ignore liabilities beyond a user's spot balance and does not cover how assets can be used or encumbered after the snapshot is taken. This is a structural problem, not an edge case.

Consider the snapshot timing issue in detail. A platform could bolster its reserves immediately before a scheduled audit by temporarily moving assets into audited wallets and withdrawing them shortly after. This is sometimes called "window dressing," and while it may not be fraudulent in a strict legal sense, it renders the snapshot meaningless as an ongoing safety guarantee. Users who trust a PoR published in January have no assurance about the platform's asset position in March.

The liability exclusion problem is equally significant. A genuine solvency assessment compares assets to obligations. If a platform holds 100,000 BTC but owes users, lenders, and counterparties 130,000 BTC worth of obligations, it is insolvent regardless of the impressive asset figure on its reserve page. PoR does not address this. It tells you the numerator without the denominator.

Asset encumbrance refers to situations where assets that appear on a reserve page are already committed to something else. For example, platform reserves might be posted as collateral for an institutional loan, pledged in a DeFi protocol, or subject to smart contract lock-up. The assets technically exist, but they may not be available to satisfy user withdrawals during a stress event.

The table below summarises the contrast between what PoR typically covers and what genuine solvency analysis requires:

| Feature | Proof-of-reserves | Genuine solvency analysis |

|---|---|---|

| Asset snapshot | Yes | Yes |

| Liabilities included | Rarely | Yes, required |

| Asset encumbrance | No | Yes |

| Ongoing monitoring | No | Yes |

| Audit assurance level | Limited assurance | Full statutory audit |

| Redemption conditions | Not addressed | Explicitly documented |

| Margin/earn accounts | Often excluded | Included |

The distinction between limited assurance and a full audit is also critical. A limited assurance engagement means the auditor has checked whether anything is obviously incorrect. A full audit involves positive verification. The language on most PoR pages implies rigour without confirming audit depth, which is a meaningful gap. Understanding trust score methodology helps contextualise why Crypto Watchdog evaluates platforms on a broader set of criteria rather than relying on self-reported reserve pages.

Pro Tip: When reviewing a PoR page, look for the exact engagement language used by the third-party firm. Phrases like "we performed agreed-upon procedures" or "limited review" carry far less weight than a full audit opinion. The difference matters enormously if the platform faces a solvency event.

The withdrawal testing importance cannot be overstated in this context. A reserve page can be technically accurate and operationally irrelevant at the same time, because what matters ultimately is whether you can move your funds when you need to.

Regulation, legal rights and how claims really work

Given the technical limitations, understanding the legal and regulatory landscape clarifies how claims translate into actual financial rights, and the picture is more sobering than most platforms let on.

The SEC statement on stablecoins argues that retail stablecoin holders generally lack a direct redemption right against the issuer, which means they have no guaranteed access to the reserve to enforce redemption. Instead, most retail users hold an unsecured creditor position, meaning that in a bankruptcy scenario, they join a queue behind secured creditors with a lower probability of full recovery.

This is a profound legal distinction. Consider the difference between owning gold in a vault and holding a paper claim that says you are entitled to gold. The first gives you direct property rights; the second makes you a creditor of whoever manages the vault. Most crypto platform claims operate far closer to the second model, yet they are marketed with the confidence of the first.

The practical implications for traders and investors are significant:

- Reserve backing does not equal redemption rights. A stablecoin or platform may hold sufficient reserves on paper, but the mechanism for accessing those reserves during a crisis may not exist for retail users.

- Regulatory status does not confer insolvency protection. Being registered with or licensed by a financial authority may impose operating standards, but it does not guarantee fund recovery if the platform becomes insolvent.

- Unsecured creditor status is the common outcome. In most platform bankruptcy cases, users with funds on exchange or in stablecoin positions become unsecured creditors, which historically leads to partial or no recovery.

- Terms of service override marketing claims. A platform may claim full backing while its terms of service include clauses that limit liability, allow rehypothecation, or restrict withdrawals during extraordinary circumstances.

The questions you should ask before using any crypto platform include a direct interrogation of its terms regarding user fund segregation, insolvency procedures, and the specific legal nature of the claim you hold over your deposited assets.

| Claim type | What users assume | Legal reality |

|---|---|---|

| Proof-of-reserves badge | Platform is solvent and safe | Assets exist at a moment; liabilities excluded |

| Stablecoin full backing | Redeemable 1:1 at any time | Retail users often lack direct redemption rights |

| Regulatory licence | Funds protected by authority | Licence imposes standards, not recovery guarantees |

| Third-party audit seal | Independent financial verification | May be limited assurance only |

| Insurance fund | Losses covered automatically | Coverage is capped, conditional, and often opaque |

Checklist for evaluating claims and platform safety

Armed with regulatory context, it is time to convert this understanding into practical due diligence steps you can apply before placing funds on any platform.

Do not treat PoR badges or reserve pages as equivalent to solvency audits. The checklist below is designed to help you ask the right questions systematically, addressing the four core dimensions that matter most: liability inclusion, audit depth, asset availability, and snapshot timing.

- Verify what liabilities are included. Ask whether the PoR or reserve report covers user liabilities across all account types, including earn products, margin positions, and institutional lending. If only spot balances are shown, the picture is incomplete by design.

- Establish the assurance level. Determine whether the engagement was a limited review, agreed-upon procedures, or a full statutory audit. The difference in assurance depth is substantial, and platforms that do not clarify this are worth treating with additional caution.

- Investigate asset encumbrance and availability under stress. Ask whether published reserve assets are subject to lock-up periods, pledged as collateral, or deployed in yield strategies that could restrict withdrawal during market volatility.

- Scrutinise snapshot timing. Check how frequently reserve data is updated. A quarterly snapshot is far weaker than real-time or daily reporting, and platforms that publish infrequently leave long windows during which conditions may deteriorate.

- Assess withdrawal history and operational behaviour. A platform that has restricted withdrawals in the past, even briefly, should carry a permanent caution flag. Operational behaviour during stress events tells you more than any reserve page.

Pro Tip: Before depositing meaningful capital, conduct a small test withdrawal during a period of normal market activity. This practical step, which we carry out in all our platform assessments, gives you first-hand evidence of operational reliability rather than reliance on self-reported claims.

When vetting new tokens or platforms, apply the same scrutiny to tokenomics claims as to reserve data. A vesting schedule is only as reliable as the governance structure enforcing it. Similarly, wallet analysis for transparency gives you on-chain evidence that you can verify independently, rather than relying on what the platform publishes. If you hold assets in a self-custody wallet, verifying wallet safety is the next logical step to ensure your personal security posture matches your due diligence of the platforms you interact with.

What most guides get wrong and how to truly safeguard your funds

The conventional guidance in this space tells you to look for audited reserves, regulated status, and well-known backers. That advice is not wrong, exactly. It is just incomplete in ways that cost people real money.

Here is what we have observed repeatedly: platforms can satisfy every standard checklist item and still fail. FTX had prominent institutional investors, a recognisable compliance posture, and widespread industry credibility. What it did not have was a genuine separation between user assets and operational funds. No badge or PoR page captured that risk, because the risk lived in the behaviour of the people running the platform, not in its published documentation.

The harder truth is that regulatory assurance means very little without practical withdrawal access. A licence tells you a platform met a standard at a point in time. It does not tell you whether you can withdraw your funds tomorrow. We have reviewed platforms where the compliance documentation was pristine and the actual withdrawal process was unreliable, slow, or subject to sudden unilateral restrictions.

Our hard-won lesson, across dozens of crypto reviews and audits, is this: verify operational withdrawal first, then look at the documentation. If a platform processes test withdrawals promptly, transparently, and without friction, that is a meaningfully stronger trust signal than any transparency badge. If it introduces delays, requests unusual identity steps, or restricts amounts without clear explanation, no audit certificate changes that risk profile.

The industry narrative focuses on what platforms publish. We focus on what they actually do. Those two things are often very different, and the gap between them is exactly where losses occur.

Safeguard your investments with independent reviews

Stepping beyond advice, staying protected in practice means having access to ongoing, independent intelligence about platform behaviour, not just reading a single report and moving on.

At Crypto Watchdog, we apply a rigorous 8-point audit framework to exchanges, wallets, DeFi protocols, and trading platforms, covering deposit and withdrawal reliability, security architecture, claims versus actual performance, and team transparency. Our trust scores give you a grounded, evidence-based view of where a platform sits on the safety spectrum. We have also published timely warnings on incidents such as the Hedgey Finance exploit, the Condo memecoin rug pull, and the Gull Network phishing attack, giving traders the early warning information they need before capital is committed.

Frequently asked questions

Does proof-of-reserves guarantee my funds are safe on a crypto platform?

No. Proof-of-reserves shows that assets existed at a single moment but does not cover liabilities or whether those assets remain available and unencumbered, making it an incomplete safety measure on its own.

What is the difference between reserve backing and redemption rights on stablecoins?

Reserve backing means an issuer holds assets corresponding to circulating supply, but retail stablecoin holders generally lack a direct redemption right against those reserves, placing them as unsecured creditors rather than collateral-backed claimants in insolvency scenarios.

How can I identify if a platform claim is genuinely trustworthy?

Look beyond badges by checking whether the platform discloses its full liabilities, specifies the assurance level of any third-party engagement, describes asset encumbrance and withdrawal conditions, and publishes reserve data with meaningful frequency rather than infrequent snapshots.

Is regulatory status enough to secure my crypto assets?

Regulatory status may impose operating standards and improve oversight, but it does not guarantee fund recovery, protect against insolvency risk, or ensure you can withdraw your assets under all market conditions.

Recommended

- Understand crypto deposit risks and protect your funds | Crypto Watchdog

- Demystifying crypto platform transparency for safer trading | Crypto Watchdog

- Why Avoid Risky Crypto Services: Protect Your Investments | Crypto Watchdog

- Protect your crypto: spot and report scams with confidence | Crypto Watchdog

Disclaimer

This content is for informational purposes only and does not constitute financial advice. Always do your own research.

Related guides

What is copy crypto trading: your 2026 guide

Discover what is copy crypto trading in our 2026 guide! Learn how to mirror expert trades safely and potentially boost your income.

TradingCrypto trading bot audit: step-by-step guide for safe trading

Learn how to audit your crypto trading bot with our step-by-step guide. Spot risks, verify performance metrics, and trade with greater confidence and safety.

TradingAI Trading Bots & Agents in 2026: What They Can and Can't Do

A calm, evidence-led guide to automated crypto trading in 2026. Where bots genuinely help, where "AI agent" marketing crosses into Ponzi territory, the regulator cases proving it, and a custody-first checklist to protect your money.

TradingThe Hidden Costs of Crypto Leverage for Beginners: More Than Just Margin Calls

Daily crypto safety insight: The real cost of crypto leverage trading for beginners

ExchangesDemystifying crypto platform transparency for safer trading

Uncover the truth about crypto platform transparency explained. Learn how to secure your assets and trade safely in 2026's market.

EducationUnderstand crypto casino risks: Essential safety insights

Uncover what is a crypto casino risk. Learn essential safety insights to protect your funds and navigate the complexities of crypto gambling.